Unraveling The Mystery Of Stock Prices

Here’s a simple method you can apply to interpret financial charts. It uses classical statistics as well as a number

Uncategorised

Displacement issues

Q: TradeStation, Ninja Trader and other trading platforms allow showing indicators with some displacement against original price chart. How we

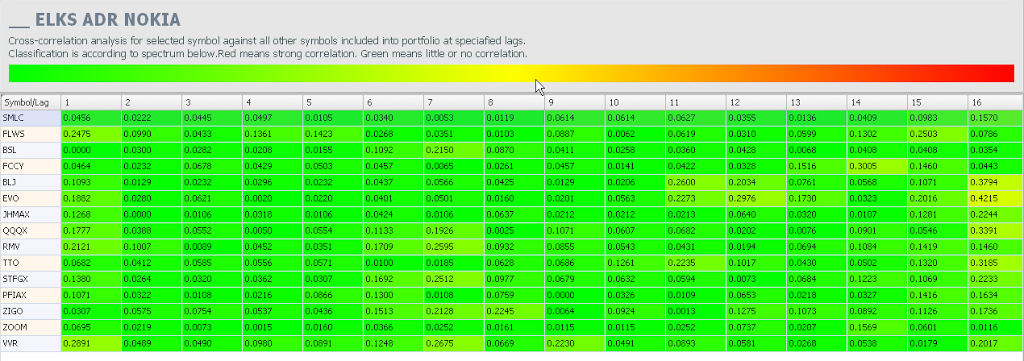

Lag correlation analysis

StockFusion Studio includes the powerful lag correlation matrix for discovery of symbol dependencies. It calculates cross correlation of selected symbol

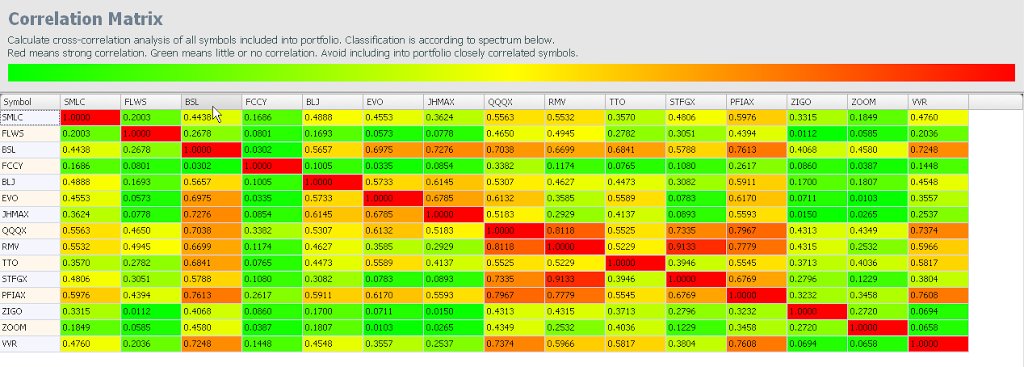

Portfolio correlation matrix

Portfolio correlation matrix is the powerful tool for your portfolio optimization. It allows optimal portfolio balancing be excluding from it

Uncategorised

Adding new symbols to symbol lookup list

It may eventually happen that your favorite symbol is not present in our Yahoo symbol lookup database, for example, due

Uncategorised

Yahoo exchanges

StockFusion Studio supports all world exchanges EOD data free of any subscription fees with its new Yahoo data provider. All

Uncategorised

The accuracy of trading performance back testing

Even beginner trader is well aware how important is testing of trading strategy on historical price data to estimate its