Walk forward test

Q: We all know that future performance does not resemble past performance. If I have found a good trading model […]

Featured news

Q: We all know that future performance does not resemble past performance. If I have found a good trading model […]

Q: I am not sure about the proper means to assess the quality of a trading model (algorithm plus trading

Q: Some algorithms in user guide are referred as predictors, others – as indictors. What is the difference between these

Q: We run your system several times on the same or slightly changed input data and obtain the results, which

Q: User manual gives special table of allowed input lengths for each algorithm. Why different algorithms require different length of

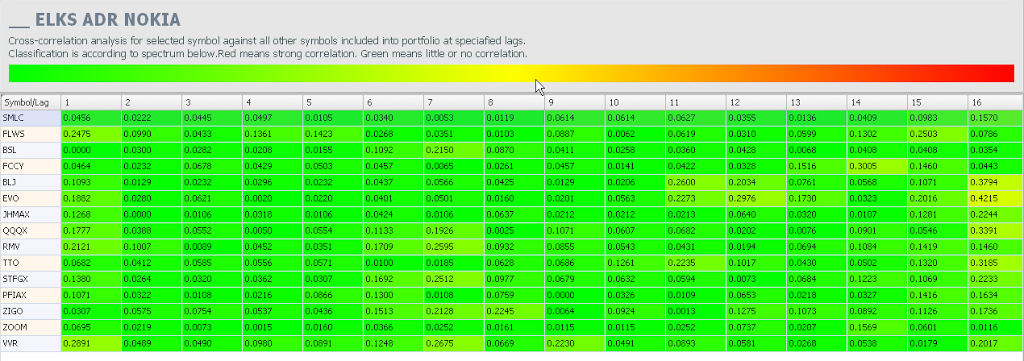

StockFusion Studio includes the powerful lag correlation matrix for discovery of symbol dependencies. It calculates cross correlation of selected symbol

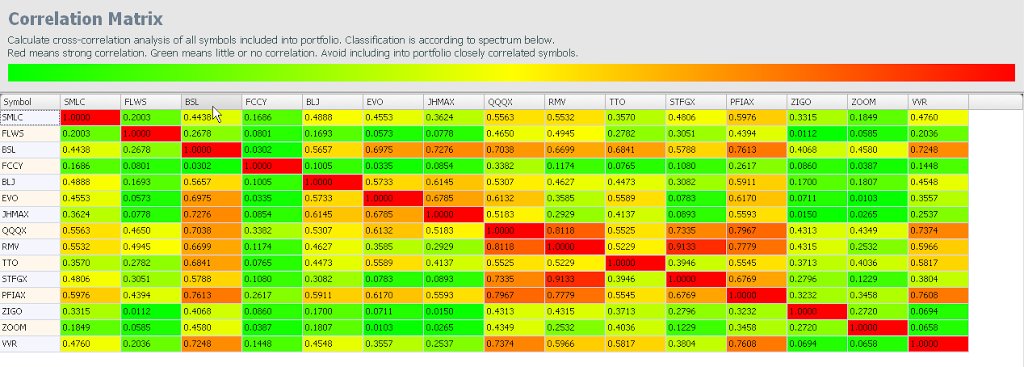

Portfolio correlation matrix is the powerful tool for your portfolio optimization. It allows optimal portfolio balancing be excluding from it